Climate Risk Consulting

Climate Change Is Accelerating, Regulations Are Rapidly Evolving With A Sharpened Focus And Investor Interest Is Intensifying

"Climate Change is Accelerating, Bringing World ‘Dangerously Close’ to Irreversible Change"

New York Times

This was the headline in a New York Times article first published in December 2019 and updated in January 2021. The headline captures the urgency, the criticality and the potential irreversibility of our climate change situation.

Our Carbon Footprint Is The Root Cause of Our Climate Change Problem

Current estimates of our collective global carbon footprint (our global GHG emissions) has shown that we are way off target. This sentiment was echoed by Antonio Gutteres, UN Secretary General in February 2021, when he acknowledged that while good progress has been made over the past year, it is not enough.

“The world remains way off target in staying within the 1.5-degree limit of the Paris Agreement”, Mr. Guterres told ambassadors.

“This is why we need more ambition, more ambition on mitigation, ambition on adaptation and ambition on finance". Describing 2021 as “a crucial year in the fight against climate change”, the Secretary-General added that the global coalition to make net zero emissions a reality needs to grow to cover more than 90 per cent of all carbon entering the atmosphere, underscoring a UN priority.

What Are Climate Risks?

Climate-related financial risks or climate risks are the financial risks linked to climate change. Climate risks can impact balance sheets and lead to losses through standard channels such as diminished asset valuations or increased loan defaults.

Central banks and financial regulators around the world recognize that climate change is a source of risk to the stability of the global financial system.

A growing number of governments are converging on a goal of net-zero emissions by 2050, in line the Paris Agreement of 2015 to keep the average global temperature rise “well below 2°C above pre-industrial levels” and to “pursuing efforts” to limit the rise to 1.5°C (UNFCCC, 2015).

They also agree that the pricing of climate-related risk with its specific challenges (including lack of relevant historical information, nonlinear nature and long-term characteristics), is a challenge for corporations, financial institutions and the financial markets.

Accordingly, there is a need for better data as well as new disclosures to better understand and manage these climate-related risks.

Click to learn more about climate risks.

Task Force on Climate Related Financial Disclosure (TCFD)

The concept of ‘climate risk’ has stemmed largely from a combination of financial regulators and private sector institutions. The Task Force on Climate-related Financial Disclosures (TCFD) has been particularly influential in helping us think through climate-related risks.

Looking at climate through a risk lens can help us understand how climate risks transmit into the real and financial economies impacting companies, countries and households and the financial institutions that lend to and invest in them and how different sectors are differentially affected.

Climate risk has two broad categories: physical risk and transition risk. Physical risks arise from the physical climate (and weather) impacts that result from the changing climate. Physical risks are subdivided into acute and chronic risks or hazards. Transition risks arise from the economic transformation needed to drastically reduce, and eventually eliminate, net greenhouse-gas emissions and reach net-zero emissions. These are outlined in the following:

Physical Risks

| Type | Examples |

|---|---|

| Acute | Increased frequency and severity of extreme weather events (e.g. wildfires, cyclones, hurricanes, floods) |

| Chronic | Increased and extreme changes in weather patterns Temperature increases Sea level rises |

Transition Risks

| Type | Examples |

|---|---|

| Policy & Legal | Introduction of a carbon tax (pricing of GHG emissions) Increased emissions reporting requirements Increased regulation of existing products or services requirements Increased permitting restrictions Exposure to legal claims |

| Technology | Cost to transition to lower emissions technology Failure of new technology and resultant loss of investment Product substitution for lower emissions products (and therefore reduced demand for existing products) |

| Market | Increased cost of raw materials Increased costs due to supply chain changes or disruption Changing customer behavior |

| Reputation | Changes in consumer perception or preferences Stigmatization of sector (e.g. extractive sector) Increased stakeholder concernNegative external feedback (e.g. social media, press) |

What Is Their Impact?

According to the Organisation for Economic Co-operation and Development (OECD), with no further mitigation actions, global temperature rises of 1.5-4°C may lower global real GDP by 1.0-3.3% by 2060 and by 2-10% by 2100. Even at the lower end of estimates, this represents trillions of dollars.

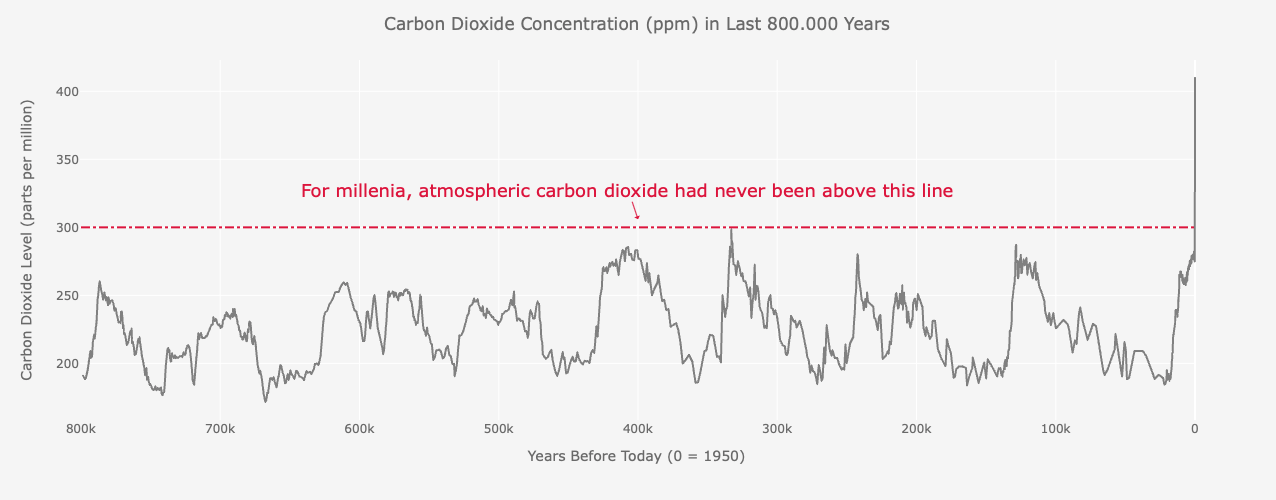

Global temperatures are rising and are now at their highest since records began. The 20 warmest years on record have been in the past 22 years. Much of the increased global temperatures have been absorbed by the oceans where we see rising ocean-surface temperatures which have led to an increased frequency and intensity of extreme weather events.

Manifestations of this include:

- In 2020, wildfires, hurricanes and other natural disasters cost more than $250 Billion of losses globally, more than thirty percent higher than in 2019.

- Six of the ten costliest events were in the USA and were largely attributable to unusually warm ocean surface temperatures.

- The ice melt in Greenland and in the Antarctic has and will continue to cause sea levels to rise.

- Wildfires are more prevalent and wildfire seasons are months longer.

What is the TCFD?

The Taskforce on Climate-Related Financial Disclosure (TCFD) was established in 2015 by the Financial Stability Board (FSB), a body established by the G20. The TCFD was charged with developing a set of voluntary, consistent disclosure recommendations that companies could use to provide information about their climate-related financial risks.

TCFD is a robust framework for organizations to use in helping them disclose their climate-related risks. This information that organizations disclose is designed to focus on the aspects of climate change that are material for financial stakeholders.

The TCFD does not impose any specific methodology regarding how to address climate risk. To quote the TCFD Technical Guide “An investor’s climate policies and practices cannot therefore be said to be ‘compliant’ or ‘in line’ with TCFD recommendations. Rather, an investor can report on its progress in implementing a climate-related policy in line with the TCFD’s recommended disclosure”.

Why Do Organizations Need Help Assessing Their Climate Risks?

“Climate change: can the insurance industry afford the rising flood risk? Floods were once considered too irregular to insure against. But global warming has changed the calculation”. Financial Times, February 2020

As transverse risks, climate-related risks will manifest themselves through the traditional risk channels or risk types. Unlike traditional risk types, climate-related risks are relatively new and not broadly well understood. This is compounded by the lack of historical data and their non-linear nature.

Risk frameworks have been developed to help organizations approach their climate-related risk assessment and disclosure requirements, the most widely used and recognized, and most likely to be adopted as the global standard, is from the Task Force on Climate-related Financial Disclosure (TCFD). TCFD presents its framework across the four areas of Governance, Strategy, Risk Management, and Metrics and Targets.

Since its launch in 2017, the TCFD has seen:

- Accelerated adoption which is expected to continue into 2022 and beyond.

- Significant growth in supporters. Currently, about half of its 2,600 supporters represent FIs, reflecting the Financial Stability Board (FSB’s) strategy that the Finance Industry plays a critical role in ensuring that global finance flows are aligned with the Paris agreement.

- Increasing government support. Until 2021, governments and regulators had not demonstrated a willingness to mandate TCFD, however, this changed significantly in 2021 with several governments around the world mandating TCFD for all or significant parts of industry within their jurisdiction.

Contact us with any questions on your climate risk needs.

We provide a range of Climate-related (TCFD) Initial Evaluations

We typically recommend an initial Evaluation for your organization. This provides you with a very quick but thorough analysis of your organizational readiness to manage your climate-related risks. We have these evaluations for Financial Services and non-Financial Services. For non-Financial Services, we have assessments for carbon sensitive industries and non-carbon sensitive industries.

Our Approach

Step 1

Contact us and schedule a meeting with one of our consultants

Step 2

Complete one of our online evaluation

Step 3

You’ll receive your detailed report within 48 hours

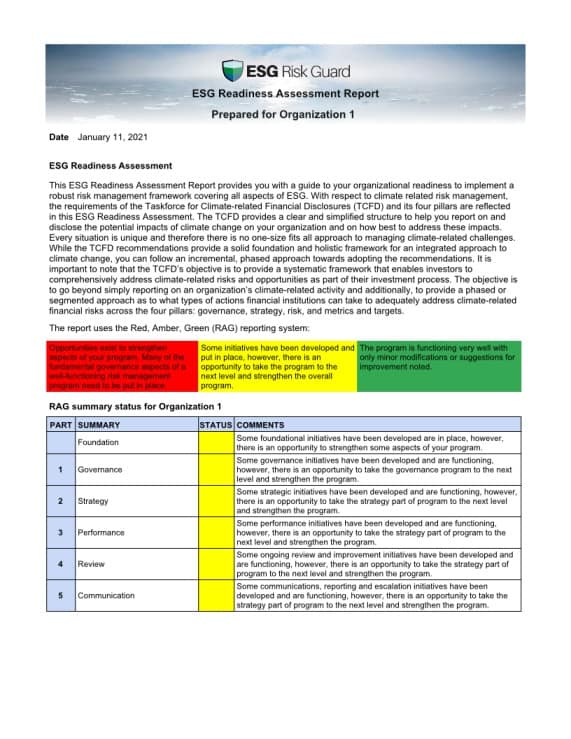

Within 24 hours of completing the evaluation, you will receive an Initial Evaluation Report based on your responses to the online questionnaire. This provides you an outline of your organizational preparedness to manage ESG or climate-related risks and tells you what needs to be done along the key dimensions of: Governance, Strategy, Risk Management and Metrics & Targets. This report will be your guide as you develop your roadmap and thereafter report on and manage your climate-related risks.This report will be your guide as you develop your roadmap and thereafter report on and manage your ESG / climate-related risks.

We provide a range of Climate-related (TCFD) Initial Evaluations

Financial Services

- Banks

- Insurers

- Asset Owners

- Asset Managers

Our financial services assessments specifically look at whether your organization has any business arrangements or interests in (including holdings in, investments in, contracts with, or loans to) carbon sensitive industries. We undertake this analysis to determine your organizational exposure to Transition risks.

Non-Financial Services

Carbon-sensitive industries: these include industries such as:

| Coal | Metals & Mining |

| Oil & Gas | Chemicals |

| Electric Utilities | Construction & Materials |

| Air-freight | Automobiles & Components |

| Air transportation | Agriculture |

| Maritime transportation | Beverages |

| Rail transportation | Packaged Foods & Meats |

| Trucking services | Paper & Forest Products |

| Real Estate Management & Development |

Operating in one of these sectors or having a business arrangement or interest in a carbon-sensitive industry increases the possibility of your organization being exposed to Transition risks.

Contact Us

Latest Articles